Collateral Fragility

How Stablecoins and Crypto Volatility Are Rewiring the U.S. Treasury Market

August 19, 2025

Introduction: Cracks in the Risk-Free Bedrock

U.S. Treasuries have long served as the ultimate safe-haven asset and global collateral benchmark. But deep, structural shifts are undermining their foundation — including a retreat by foreign central banks, saturated dealer balance sheets, and an influx of price-sensitive, crypto-linked buyers.

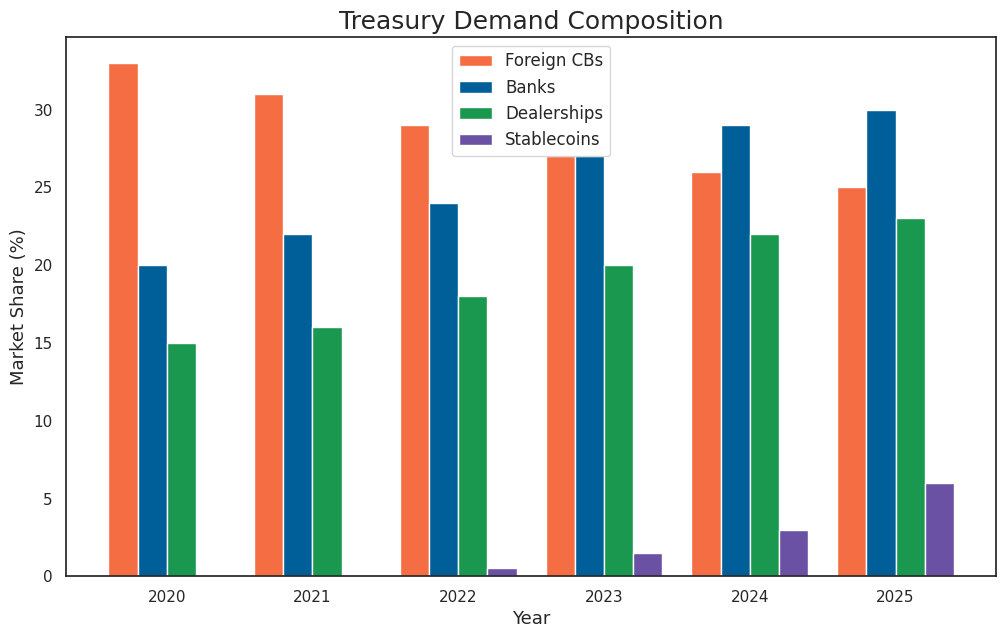

1. Demand Composition: The Decline of the Inelastic Buyer

Foreign central banks’ share of Treasury holdings has dropped from 33% to 25%, replaced by domestic banks, dealers, and notably, stablecoin issuers — now 6% of the market. Unlike traditional buyers, stablecoin demand is tethered to volatile crypto flows, introducing procyclicality and liquidation risk.

2. Dealer Constraints: Capacity Nearing the Limit

SLR utilization for primary dealers is at 95%. This regulatory ceiling means dealers are losing their ability to absorb issuance and provide liquidity — a key fragility in auction dynamics and secondary markets.

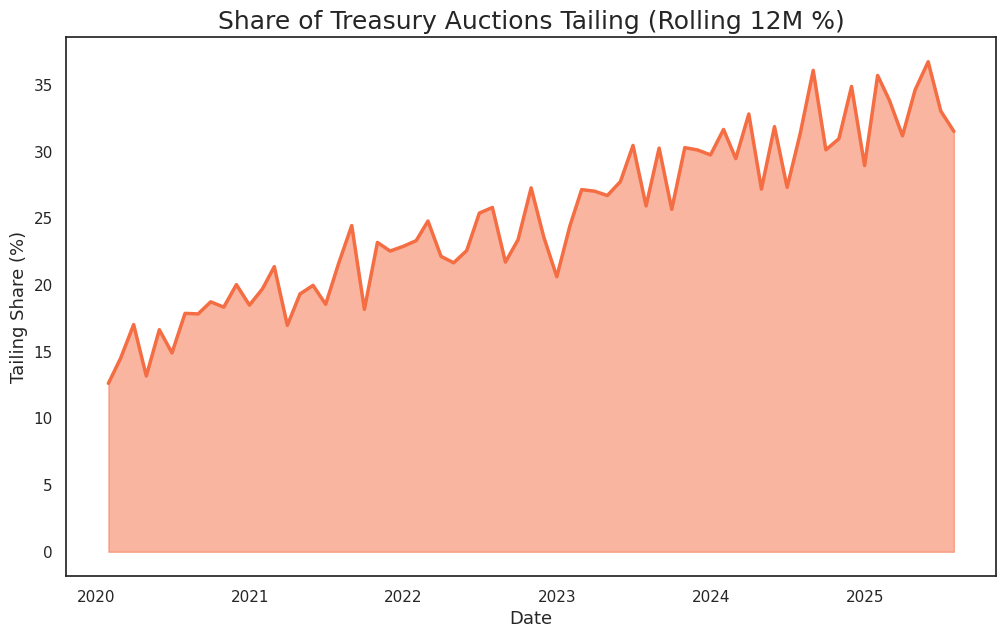

3. Tailing Auctions: A Warning Sign

The percentage of Treasury auctions tailing has climbed from 15% to 35%. This suggests structural demand weakness and growing difficulty in clearing supply without yield concessions.

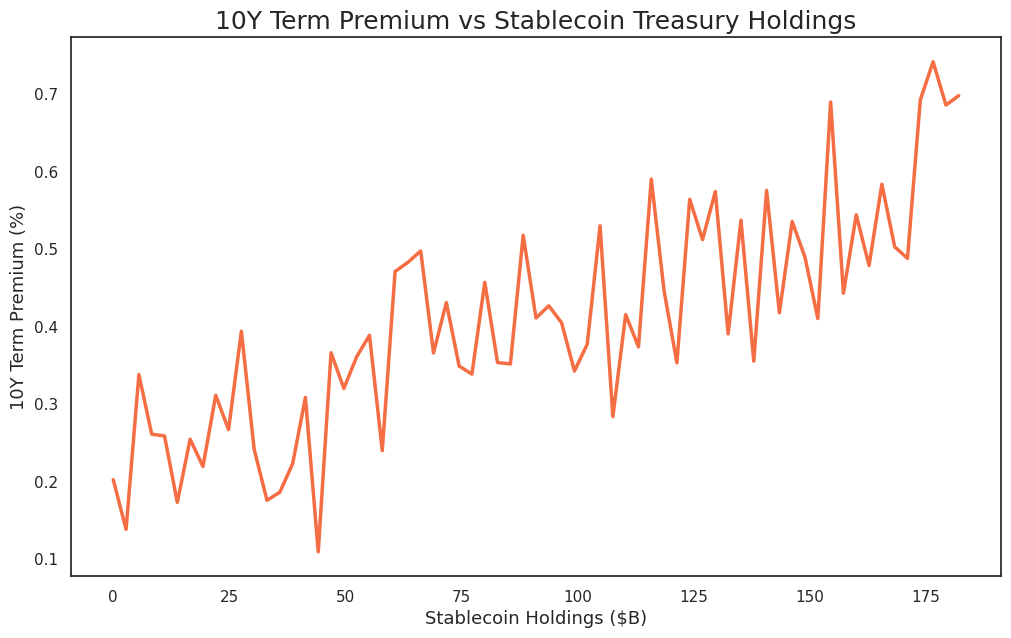

4. Term Premium Repricing

A growing correlation between stablecoin T-bill holdings and the 10Y term premium indicates a bifurcated curve: short-end yields are suppressed by crypto demand, while the long end requires elevated risk premiums.

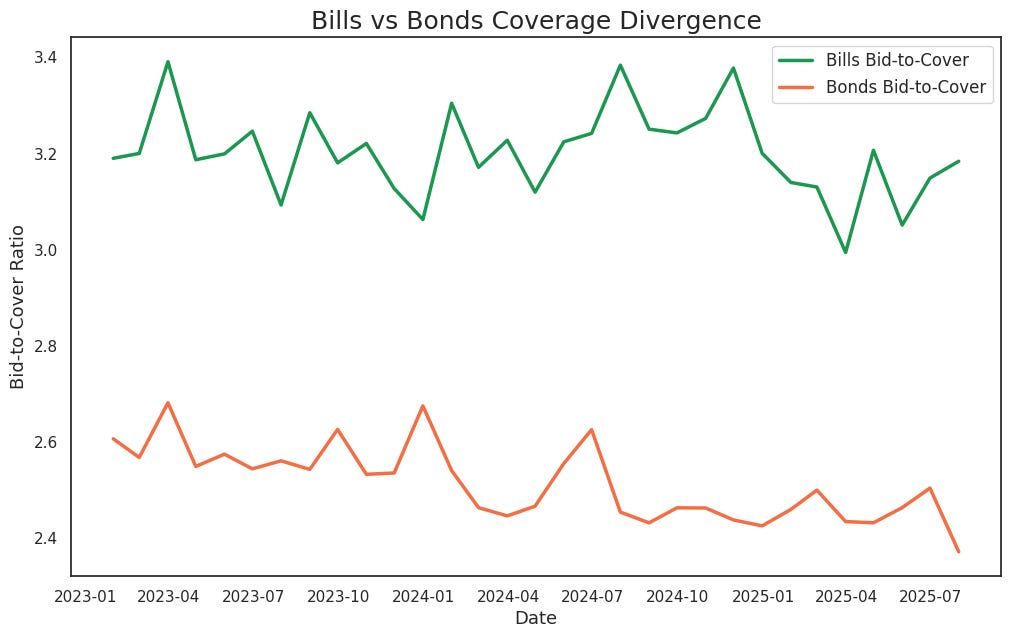

5. Front-End Strength, Back-End Erosion

Bid-to-cover ratios remain robust for T-bills (~3.2x) but are weakening for bonds (~2.4x). This divergence hides long-term risk beneath short-term strength — a fragile equilibrium.

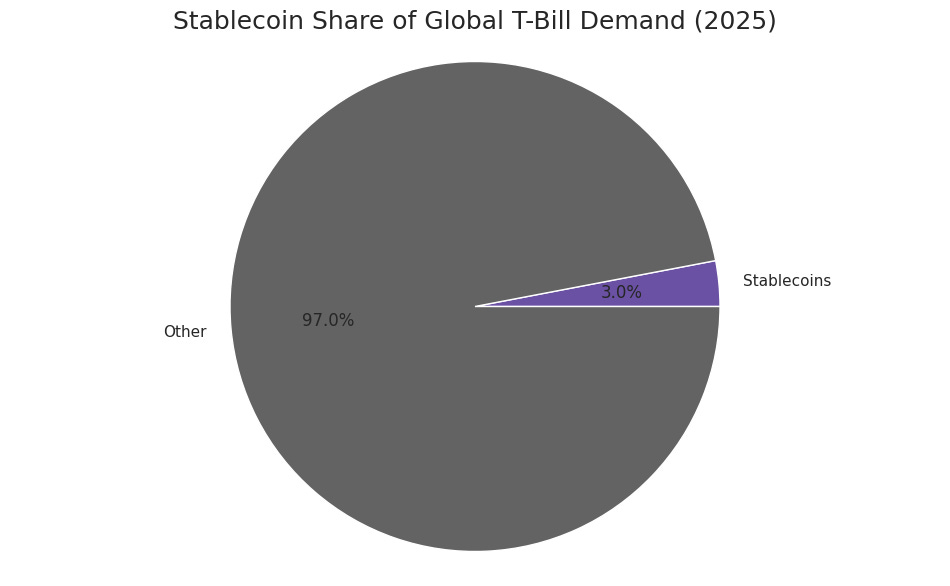

6. Stablecoins: The New Marginal Buyer

Stablecoin holdings now represent an estimated 3.0% of global T-bill demand, a rapidly growing segment absorbing short-term issuance but also contributing to collateral scarcity dynamics.

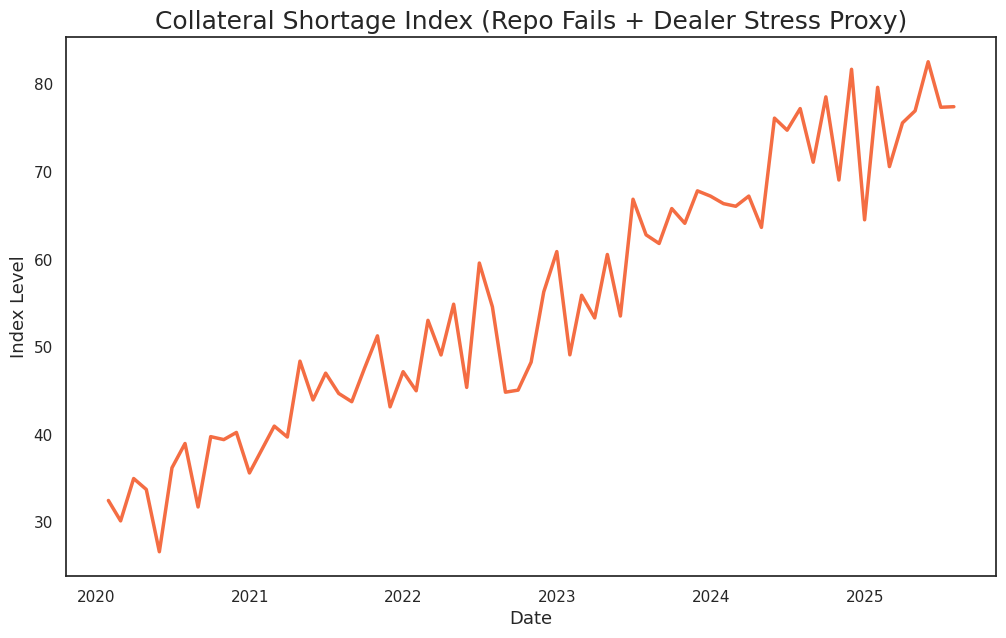

7. Collateral Stress Resembling 2019

The Collateral Shortage Index has surged from 30 to 80 — echoing the mechanics that led to the 2019 repo crisis. It’s not credit risk this time, but pure mechanical dysfunction driven by balance sheet constraints.

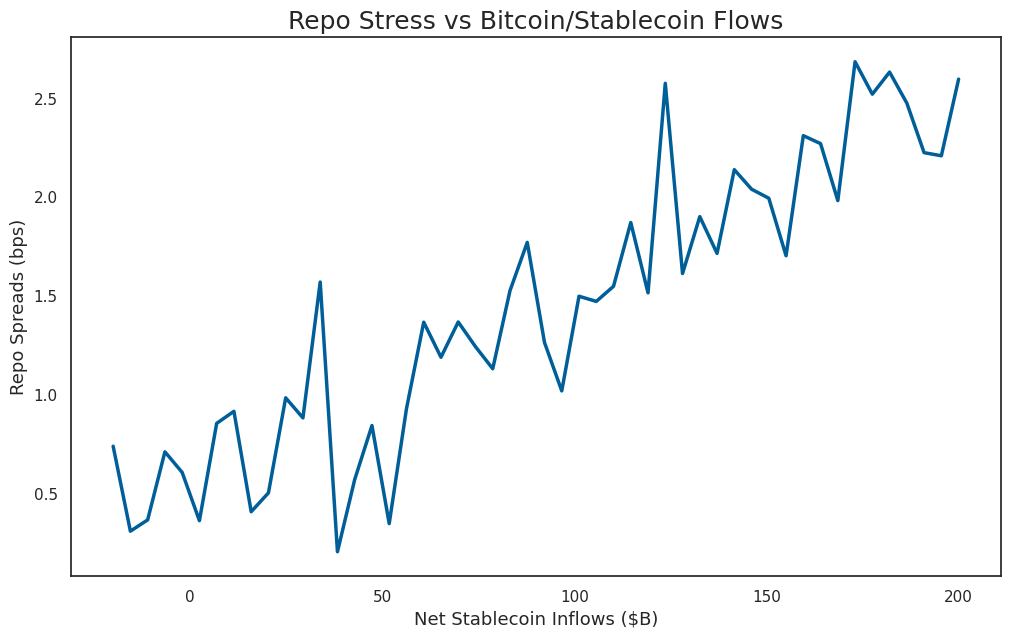

8. Repo Rates Linked to Crypto Flows

Stablecoin redemptions now affect repo spreads. A large unwind in the crypto market could forcibly remove collateral from the system, tightening funding markets almost instantly.

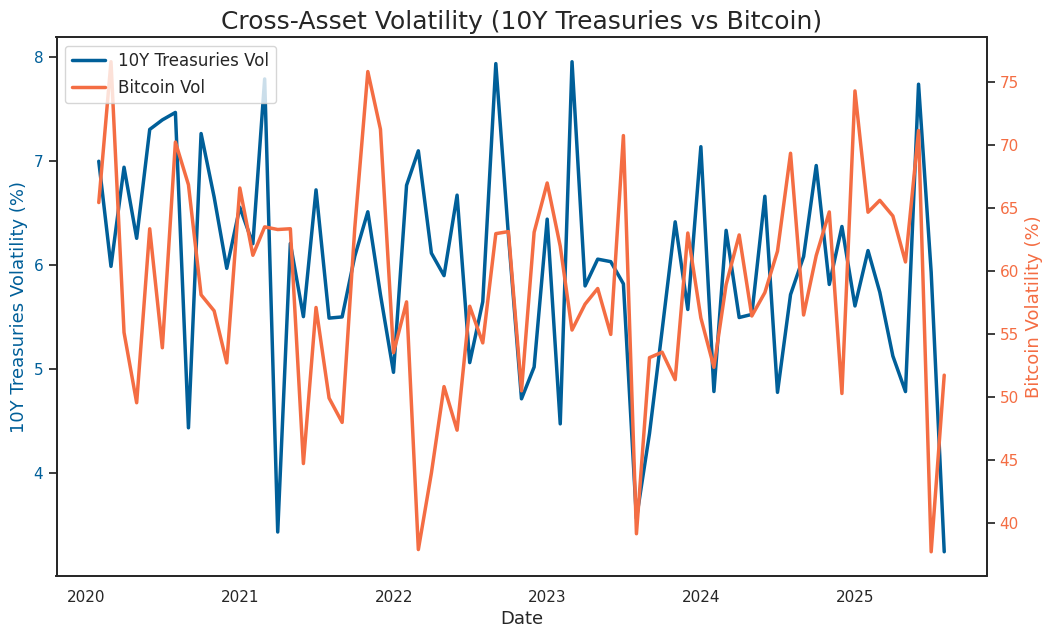

9. Volatility Spillover from Bitcoin to Bonds

Bitcoin’s 80% volatility now has a transmission path to Treasuries via stablecoin reserves. What happens in crypto no longer stays in crypto.

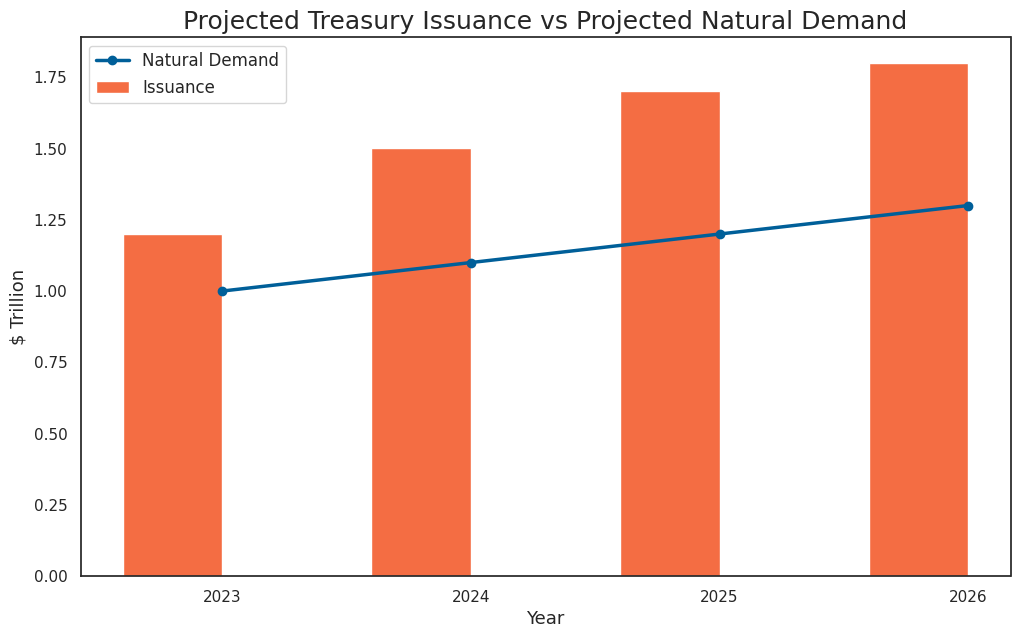

10. A Widening Structural Imbalance

Treasury issuance is projected to far outpace “natural” demand. That means increasing reliance on yield-sensitive buyers — with higher volatility and borrowing costs baked in.

11. Curve Inversion and Volatility: Signal or Noise?

As shown in the chart below, curve steepness (10Y-3M) has an increasingly inverse correlation with the VIX. Bond investors are leaning on equity vol signals — suggesting the term structure is pricing in risk offflows.

12. Collateral Richness and Front-End Arbitrage

The 3M Bill – SOFR spread has become volatile as front-end arbitrage opportunities widen. This reflects both elevated collateral demand and shifting Fed facility usage.

13. Reserve Scarcity: The QT Pressure Point

The Fed’s balance sheet run-off has drained reserves — tightening interbank funding, stressing ON RRP usage, and driving up SOFR. These constraints increasingly interact with Treasury liquidity.

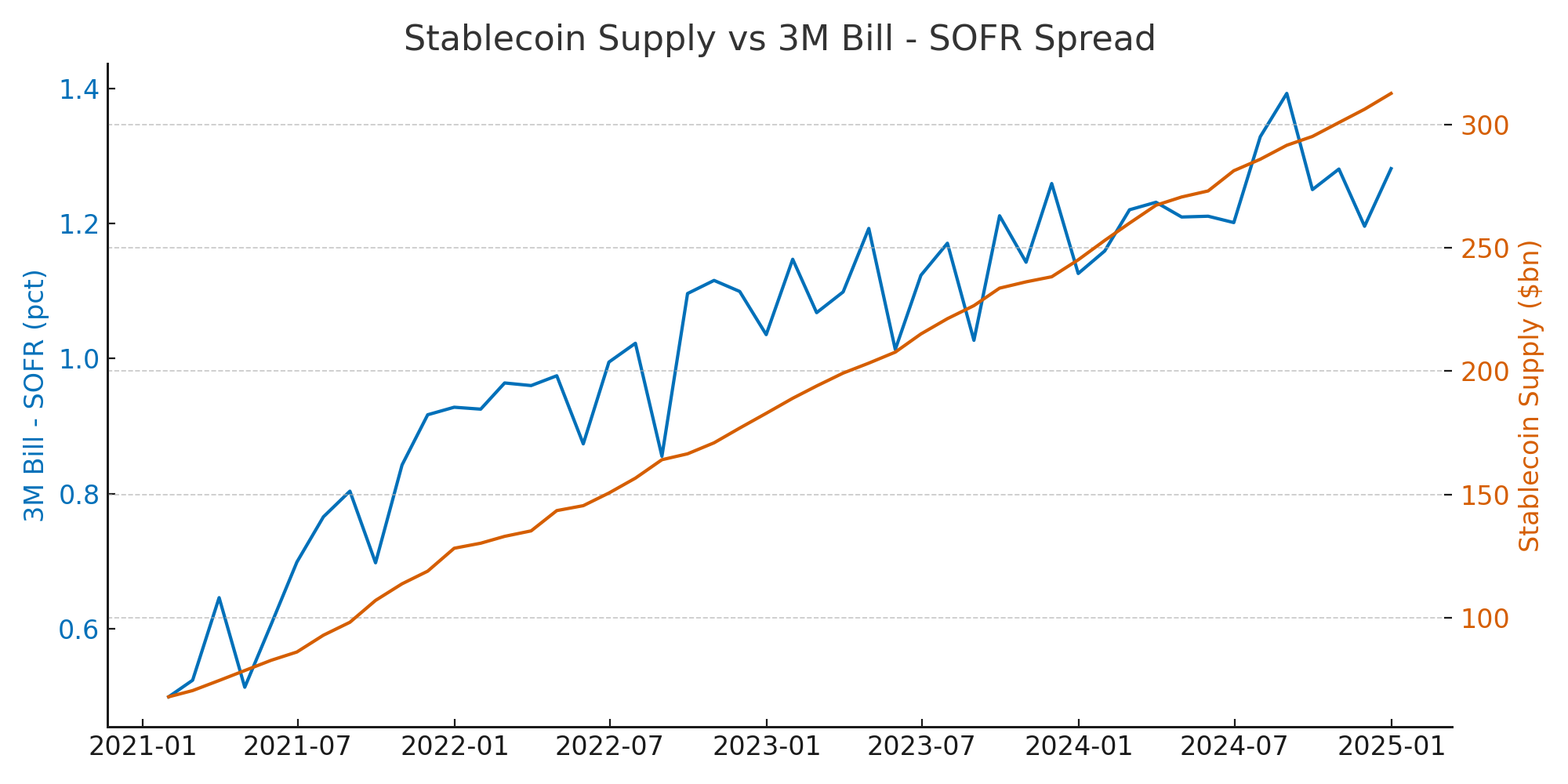

14. Stablecoin Supply vs T-Bill Richness (3M Bill – SOFR Spread)

Rising stablecoin supply correlates with richer T-bill pricing vs SOFR. Crypto-driven collateral demand is tightening front-end spreads, creating arbitrage pressures and distorting money market benchmarks.

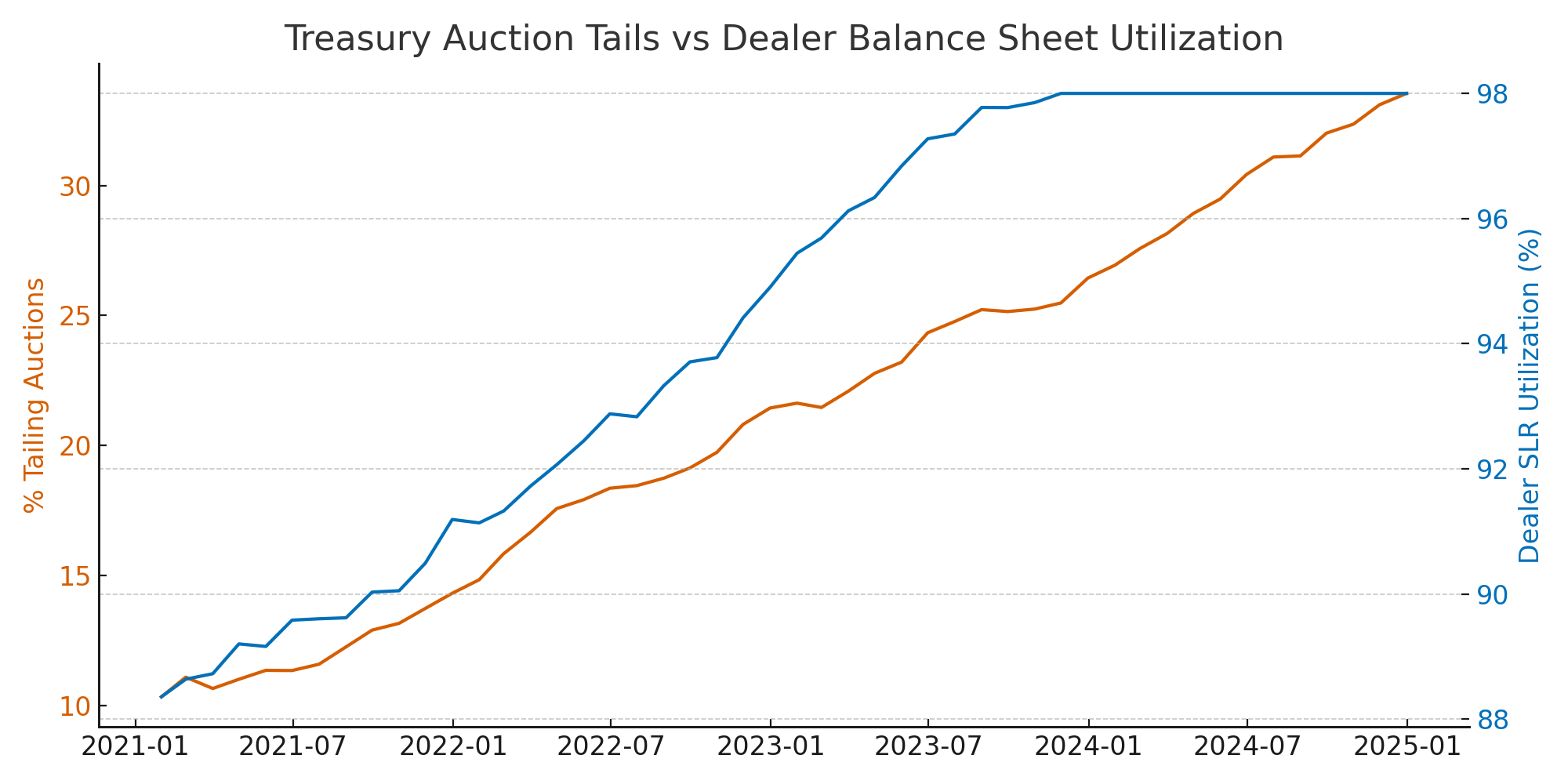

15. Tailing Treasury Auctions vs Dealer Balance Sheet Utilization

Auction tails are rising alongside stretched dealer capacity (SLR ~100%). Dealer constraints are no longer cyclical — they’re structural, impairing the Treasury market’s ability to clear supply smoothly.

Conclusion: A New Collateral Regime Has Arrived

We are no longer in a world where Treasuries are anchored by price-insensitive sovereigns and deep dealer balance sheets. The new Treasury buyer base is fractured, fast-moving, and procyclical. The result is a system prone to episodic dysfunction, amplified by macro volatility and crypto feedback loops. Collateral fragility is no longer theoretical — it’s visible in every corner of the funding market.

Great read.

Very interesting and concise - thank you.